Principales conclusiones

- The federal government taxes all lottery prizes over $5,000 at 24%, which gets deducted from your winnings.

- Larger prizes like those from Powerball and Mega Millions will shoot your taxable straight over the top federal tax rate of 37%.

- Taking the lump sum payout offers more immediate control over your prize money, while taking the annuity payout offers more security.

- Many states also tax lottery winnings, so make sure to check your state’s tax laws if you win.

- The best strategy to ease your tax burden if you win the lottery is to take the annuity payout and hire a financial advisor to help you make plans for your money.

You know how it goes, one person becomes a millionaire overnight, and the rest of America turns into financial analysts. The Powerball jackpots have been nothing short of epic in the last decade, so both the winner and the prize money themselves become celebrities for a few days (or weeks, if the prize crosses the two billion dollar mark like it did in 2022).

The thing is that, whoever wins that massive Powerball jackpot, so does the federal government. The amount of money that the winner gets to take home after taxes, and whether they should take the prize as a lump sum payout or annuity, are both topics that get endlessly dissected by us unlucky millions on the internet.

So, what’s the answer? How much in taxes does the government really take from the Powerball jackpot? Is it really better to take the annuity than the lump sum payout? What’s the best way to financially handle a millionaire prize like that (you know, in case you win)?

We will go over these topics and lay out some strategies that a lucky winner can follow to minimize their tax burden. Who knows? The next winner might stumble upon this guide.

Powerball After Taxes: How Much Of The Jackpot Gets Taxed?

Let’s say you win the Powerball jackpot (or Mega Millions, or any other lottery really). Congratulations! You’re bound to get life-changing money ten times over, right after you remember where you put that darn ticket, anyway.

So many things are rushing through your head right now: What’s the first thing you’ll buy? Your first millionaire’s vacation? But the one thing that should come first is — you guessed it — taxes.

In fact, you should also hire some people to think about taxes for you. Getting the help of a financial advisor and tax attorney to help you plan on how you’ll deal with the tax implications of your prize.

The IRS withholds 24% on all lottery winnings above $5,000 before you decide if you’ll take the prize at once or in installments.

How Powerball Payouts Work

Few prizes in this life are as eye-popping as the Powerball and Mega Millions jackpots. Still, impressive as they are, it’s pretty much a given that you never get the full amount once you win.

For starters, even before Uncle Sam gets a piece of the pie, you might have to split the winnings evenly with anyone else whose ticket matches all six numbers. Of course, each winner would have their pick of lump sum payout or annuity.

Lottery prizes are made up of ticket sales, so the reason why you’re seeing bigger and bigger jackpots each time is simply because people are spending that much more money on tickets each year.

The allure is so big that just last year, U.S. lottery players spent over $113.3 billion on lottery tickets.

If you’re concerned about privacy, be sure to check out your state’s laws on anonymity when claiming a lottery prize; some of them are legally obligated to share the identity winner along with their prize to any third party that requests that info.

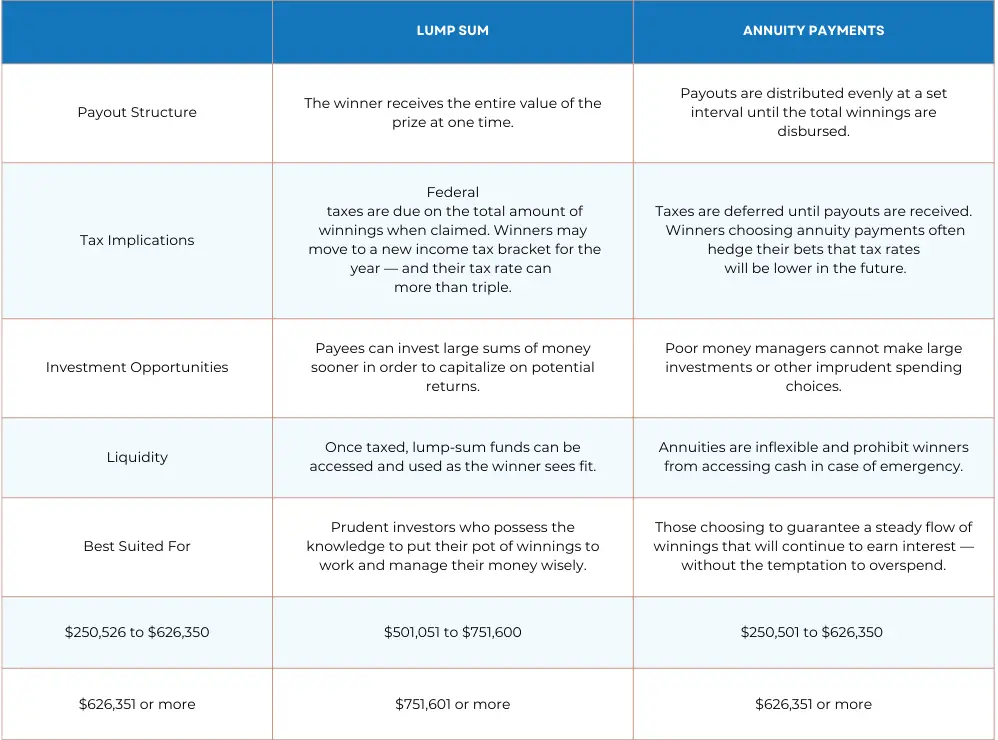

Lump Sum Payout Vs. Annuity

Contrary to what people on either side of the debate will tell you, there actually are benefits to both taking the lump sum of your winnings or choosing the annuity.

Let’s look at some facts first: The lump sum payout allows you to take control of most of your prize almost immediately once all taxes have been paid. Lottery winners all have big ideas for the money, so this is the most popular option by far.

Also, the lump sum carries less long-term tax obligations, making it more attractive for some. Perhaps the best argument in favor of taking the big payout is that it allows for immediate investments on a much larger scale compared to annuity.

On the other hand, choosing the annuity option means that you’ll get your prize money (after taxes) in annual payments, usually over a period of 29 years.

This is the only option that offers any sort of growth, since your post-taxes money pool is invested for you by the government and accrues interest over those 29 years.

The security of having a substantial, guaranteed annual payout is attractive for people who prefer the feeling of having a safety net. Another advantage is that, depending on the size of your annual payments and other income sources you might have, the annuity option might not put you right at the top of the tax bracket (if the prize is on the smaller side).

As you can see, it’s all about short-term advantages vs long-term advantages, and depends on what financial goals the winner has in mind.

Be advised, however, that most financial analysts will recommend taking the annuity as a way to protect yourself from spending the money too fast, and to take advantage of the interest it can generate.

Source: Annuity.org

How Much Do Lottery Winners Pay In Taxes

It goes without saying that winning a big prize means you owe the government big taxes. However, just how much you owe depends on a couple of factors, including which type of payout you chose and how you’ll file your taxes for that year.

There are four main factors that affect how your prize money will be taxed:

- Total Lottery Winnings: First of all, obviously, is that a bigger prize will carry a bigger tax burden. A large enough jackpot will push you into a higher tax bracket, which will affect not only your prize money but the entirety of your taxable income.

- Lump Sum Vs. Annuity: Whatever payout method you choose to receive your prize will change how much you’re taxed on it. A lump sum means paying a bigger chunk of change upfront, while annuity spreads it out along with the prize.

- State Where You Purchased The Ticket: State tax laws on lottery winnings vary wildly across the country. There are states that exempt your winnings, but others can tax you up to 8% on them.

- Personal Income: This is more of an issue for those who choose annuity, since the annual payment combined with your regular income can push you into a higher tax bracket in perpetuity.

Let’s take a quick look at how much you’ll have to pay on federal taxes if you manage to hit a million-dollar jackpot.

Federal Taxes On Powerball Winnings

If you choose to get the prize in a lump sum, you’ll almost definitely be subjected to the top tax bracket of 37%; that is 24% + 13% for a total of 37%, not 24% + 37 percent, which would be scandalous). Now we have to think about filing statuses and their income thresholds.

The top tax rate of 37% applies to single taxpayers with an income exceeding $609,350 (for 2024), while married people filing jointly that income threshold is $731,200. On top of that, most states consider lottery cash prizes as taxable income, with different rates per state.

It’s time to show you an example, and for that we have to crunch some numbers. Suppose that you hit the jackpot of a clean $1 million dollars. Let’s see what happens if you take a lump sum payout on that prize:

- You have an initial prize of $1,000,000. The IRS automatically withholds 24% of all lottery winnings over $5,000, so that’s 24% of $1,000,000 = $240,000.

- The IRS withholds $240,000, leaving $760,000 of the prize.

- $760,000 puts you way above the highest tax bracket’s threshold of 37% for single taxpayers, and just over for joint filers.

- Remember, that doesn’t mean a 37% tax on top of the 24% they already took; in this case you just add the difference between 24% and your tax bracket, so that’s 37-24=13.

- So, you subtract another 13% off of the remaining $760,000.

- Your total prize after federal income tax: $661,200 out of the initial $1 million.

State Taxes On Lottery Winnings

You should be wary of state tax laws on lottery winnings since they can really add another layer of complexity to the whole situation. Each state has its own laws when it comes to lotteries; some states exempt lottery winnings, but most do not, and they can tax as much as 15% of your prize money.

It’s also worth remembering that lottery winnings will also push your state tax bracket up, along with the federal brackets.

If you happen to live in a state without a lottery but you purchased a winning ticket from a state that does, that state might withhold taxes on your prize money.

For example, both Maryland and Arizona will tax your lottery winnings if you bought the ticket there, even if you don’t live in either of them. Also, remember that just by living in a state that does not impose taxes on lottery winnings doesn’t mean you’re exempt from the federal tax.

How To Minimize The Tax Burden Of Winning The Lottery

Choose The Annuity Payments

We get why so many lottery winners choose the lump sum option over annuities, and while some of their reasons are valid, most of them are frankly short-sighted, to say the least. An oft quoted myth is that the lump sum is better because annuities end if the winner dies; the truth is that the prize would simply pass to the winner’s estate.

Annuities offer more long-term benefits that you can take advantage of, like the fact that the prize money itself generates interest over time, essentially growing by itself during a 29-year period.

They also give you more time to plan how you’ll deal with the future tax implications of such a large amount of money falling on your lap, and to pretty much protect the money from both yourself and others.

So, all in all, especially for the bigger prizes, annuities end up being the better choice for most winners simply because of the sheer number of advantages they offer. They give you time to set things up right so that you don’t lose it as fast as you won it.

Get A Professional To Help You Plan

Chances are that after hitting the jackpot, a million of your closest friends are going to race to ask you for a small loan, but right behind them will be the people trying to offer you unsolicited financial advice.

Winning the lottery might prove stressful if you’re not sure about what to do, so having an actual professional guiding you through the whole ordeal can save you from making costly mistakes you’ll most likely regret down the line.

Start A Foundation

Private foundations are something ubiquitous to America, and Powerball winners are in the right position to create their own. Philanthropy gives you an opportunity to do some good in society, no matter how niche the problem you’re dedicated to, and also happens to be a great way to secure (at the very least) a comfortable, upper-class life.

You see, nonprofits are very regulated by the U.S. government, from making out loans to yourself to hiring friends and family to do nothing and then cash a fat check; however, the laws regulating these situations still leave enough room to offer healthy salaries that aren’t above market. So, it’s neither fraud to “donate” money to yourself nor a get-rich-quick scheme; it’s just buying yourself the best job you’ve ever had while actually trying to do some good in the world.

Powerball Winnings After Taxes: Frequently Asked Questions

1. What percentage of my Powerball winnings will be taxed?

Your Powerball (and any other lottery winnings) will be taxed in a few different ways:

- Federal taxes: First of all, the IRS withholds 24% of the prize money upfront. Then, the money will be taxed as part of your total tax liability for the year, probably with a 37% tax rate (the highest tax bracket for 2024).

- State taxes: This one has the most variability, since each state has its own tax laws for lottery winnings. California and Florida, for example, exempt lottery winnings, while others can tax you up to 10% on them. Some states will even tax your winnings if you bought a ticket in them even if you don’t live there.

- Local taxes: Certain cities may apply local taxes.

2. What is the main difference in taxes for the lump sum vs. annuity payout?

For the lump sum payout, the tax burden will be higher because you receive the whole amount after taxes upfront, and the prize is all taxed on the year you receive it.

For the annuity payout, your prize will be given to you in annual installments, each being taxed according to that year’s tax laws but potentially keeping you in a lower tax bracket.

3. What is a legal way to reduce the taxes on lottery winnings?

Your options are limited when it comes to reducing the tax burden on lottery winnings. You can make charitable donations up to a certain amount, or set up a nonprofit corporation or trust.

You can also hire a financial advisor and/or tax attorney to help you make plans for the money. Finally, you can take the annuity payout option because it allows you to spread the tax obligations over 29 years.

4. Does gifting my lottery winnings help me avoid taxes?

No. Gifting is allowed, but the tax exemption for it is still tied to the annual exclusion amount ($17,000 per gift recipient).

5. Can I claim my lottery prize anonymously?

Staying anonymous after winning the lottery is up to the state where you live. Some will allow you to keep your privacy, but others will disclose your identity to any third party that requests the information. Keep in mind that privacy laws are completely unrelated to tax laws.

Jacob Dayan

Entrepreneur • CEO Community Tax, LLC

Jacob Dayan is the CEO and co-founder of Community Tax LLC, a leading tax resolution company known for its exceptional customer service and industry recognition. With a Bachelor’s degree in Business Administration from the University of Michigan’s Ross School of Business, Jacob began his career as a financial analyst and trader at Bear Stearns and Millennium Partners before transitioning to entrepreneurship. Since 2010, he has led Community Tax, assembling a team of skilled attorneys, CPAs, and enrolled agents to assist individuals and businesses with tax resolution, preparation, bookkeeping, and accounting. A licensed attorney in Illinois and Magna Cum Laude graduate of Mitchell Hamline School of Law, Jacob is dedicated to helping clients navigate complex financial and legal challenges.

Puede que también le guste