Principales conclusiones

- Social Security benefits becoming non-taxable after you turn 70 is a myth.

- In truth, a portion of your Social Security benefits remain taxable from the moment you start getting them until you die.

- The money you get from Social Security is treated as taxable income by the federal government, and must be reported as such on your tax return.

- On top of that, all but 12 states also tax Social Security benefits.

- There are several ways to minimize the tax burden on Social Security benefits, such as making qualified charitable distributions, and strategic withdrawals from your retirement accounts to lower your RMDs.

Is social security taxed after age 70? In life there are many myths that people keep believing despite them having no basis in reality, like chewing gum supposedly doesn’t digest, or how it’s safe to pick up and eat food that fell on the floor for less than five seconds.

Sadly, another one of those myths that just isn’t true is that social security becomes tax-free at age 70 (or 75, or even 65 for the particularly optimistic).

Unfortunate as it is, the truth is that Social Security benefits don’t just simply become nontaxable at one specific age, but it’s easy to see why many people believe it. But why is it like that? Is there cualquier age at which Social Security is finally tax free? How does it happen?

Let’s take a look at the relation between Social Security benefits, taxes, and age; then we’ll go over some of the ways in which you can actually reduce your taxes on them.

Is Social Security Taxed After Age 70?

Some retirees don’t pay taxes on their Social Security benefits per se because they simply are below the income threshold where they have to file a return. But overall, yes, a portion of your Social Security benefits are taxable from the age when you start collecting right up until you die.

“Death and taxes”, as the old saying goes, right? But it’s not as grim as it seems! Only a portion of your benefits is subject to federal taxes instead of the full amount.

Also, there’s plenty you can do to minimize your tax liability even if you can’t avoid paying taxes on your benefits.

The myth that social security stops being taxed after a certain age is sadly false, but it’s also easy to see why it keeps popping up: Retirement is a thing, after all, so if you can stop working after a certain age, wouldn’t taxes follow suit?

Perhaps in an ideal world, but the truth is that retirement is not the same for everyone. There’s also the abundance of tax benefits afforded to senior citizens (mostly for state taxes), so that might be conflated into the whole situation.

Who Has To Pay Taxes On Social Security?

These are the scenarios where you would have to pay taxes on your Social Security benefits according to IRS rules.

For these, you will need to take your combined income into account; a combined income is the result of your AGI + nontaxable interest + 50% of your Social Security benefits.

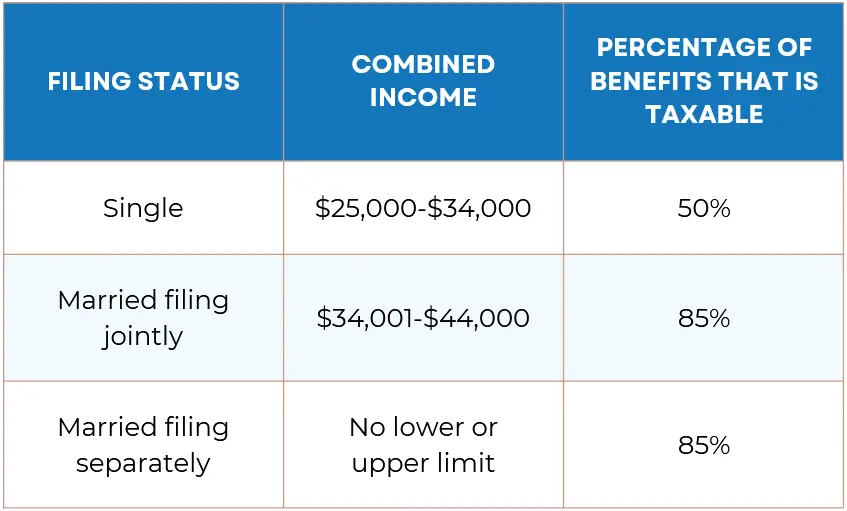

Filing As A Single Taxpayer

Filing as a single taxpayer with a combined income higher than $25,000 but lower than $34,000 will have you paying income tax on up to 50% of your benefits.

If you’re above the $34,000 combined income threshold, then you will pay income tax on 85% of your benefits.

Filing A Joint Return

If you and your spouse have a combined income between $34,000 and $44,000, then up to 50% of your benefits may be taxable, while up to 85% of them will be taxable if your combined income exceeds $44,000.

Being Married But Filing A Separate Tax Return

Just by being married and filing separately while living with your spouse at any time during the tax year will make up to 85% of your benefits taxable.

How Social Security Taxation Works

While Social Security comes from the federal government, once the money reaches your pocket it’s treated as taxable income, meaning that a portion of it will go right back to their pockets.

That’s just the way it works. Other forms of taxable income for retirees are retirement plan benefits, pensions, and all the money you make by working after retirement.

There is also the fact that, while taxation of Social Security is treated the same across the U.S. at the federal level, states are a different story. Each state has its own rules for dealing with taxes on Social Security like only taxing a portion of it, while other states simply do not tax it because they don’t have a state income tax.

Actually, this division might also play into that rumor of Social Security not being taxed at a certain point in your life.

The Relation Between Taxes And Social Security

The benefits from Social Security that are considered taxable by the IRS include monthly retirement, survivor benefits, and Social Security Disability Insurance (SSDI). Supplemental security income payments, on the other hand, aren’t taxable.

The way benefits affect your taxes is quite simple, really; since they are considered regular taxable income, they are added to your AGI and can push you into a higher tax bracket, hence why they’re such a double edged sword.

Still, retirees whose income is limited beyond just Social Security aren’t often taxed on their benefits barring very special circumstances.

As you can see, what matters is your total income and not so much your age (which does come into play with some other tax-related topics).

Retirement Income Sources

Traditionally, planning for your retirement means paving the way for multiple sources of income from which you can depend on once you stop working.

The more sources of income you have, the higher your combined income (which we will break down in a following section) will be, and that means having a bigger chunk of change taken from your benefits.

Some of these income sources are:

- Pensions: All payments from your pension are considered ordinary taxable income by the IRS.

- Withdrawals From Tax-Deferred Accounts: Distributions from regular IRA accounts, 401(k)s, and 403(b)s are all considered taxable income.

- Investment Income: All interests, dividends, and capital gains count toward your taxable income, it doesn’t matter if you reinvest it.

- Wages From Part-Time Work: Continuing to work past your retirement-age adds to your taxable income in the form of wages.

Tax-Free Income Sources

Aunque some forms of income, such as interest from municipal bonds, may seem tax free at first, they are still counted when it comes to calculating your provisional (or combined) income.

That could make the taxable portion of your Social Security benefits go up and, again, cause your Social Security benefits to be taxed at a higher rate.

Required Minimum Distributions

People born after 1950 are required, after age 73, to take RMDs from their tax-deferred retirement accounts. For people who have never withdrawn any money from those accounts previous to age 73, the RMDs can be quite substantial, which can increase their taxable income significantly.

It’s essential that, if you chose a tax-deferred account for your retirement, you should plan strategic withdrawals from them before the RMDs kick in to help reduce their impact.

Planning For Taxation After Retirement

As you have seen so far, effective planning for retirement should always include tax preparation, which includes knowing what to do about your Social Security benefits.

Diversification and timing are both the key for a successful contingency plan, allowing you to have enough money across different income sources and to avoid any unnecessary grief with taxes.

Here are a few strategies that can help you achieve just that (and the sooner you start, the better!)

Diversify Your Income Sources

There’s nothing more fruitful in old age than a well-diversified portfolio that allows you a more flexible income. In particular, you want the freedom to manage your taxable income to your benefit when tax season comes around.

Consider at least looking into taxable accounts (such as brokerage accounts), some of the tax-deferred accounts we’ve talked so much about in this guide (like traditional IRAs and 401(k)s), and tax-free accounts (which includes Roth IRAs and Health Savings Accounts.

The key is to withdraw from these accounts strategically to keep your income below the threshold.

Keep And Eye On Your Medicare Premiums

As if being taxed on your benefits wasn’t enough, a higher-income in retirement can trigger the Income-Related Monthly Adjustment Amounts (IRMAA).

Not only is their name long and scary, they also increase your premiums for Medicare Parts B and D. The key is to keep your income manageable to keep your premiums low.

Plan For State Taxes

In case you live in one of 12 states that tax Social Security benefits, you should plan for those as much as you do for federal taxes.

Understanding your state’s rules and regulations on Social Security benefits will help you minimize their effects on your pocket. But, if that seems like too much, moving to another state that’s more tax-friendly is always an option.

How To Reduce Your Taxes On Social Security Benefits

While it might be impossible (and illegal) to avoid taxes on your Social Security benefits as a whole, there are a couple of (fully legal) tricks you can do to lower your taxable income and, with some elbow grease and a little luck, reduce how much your benefits are taxed.

- Make strategic withdrawals from your retirement accounts: This strategy can be a bit of a doozy, but here’s the long and short of it. If your tax-deferred accounts are diversified enough and you time your withdrawals just right, you can lower your tax liability by avoiding higher tax brackets. You will also control the amount of taxable income in your return, and lower the required minimum distributions (RMDs) that kick in when you turn 73. As we said, it’s a complex strategy, so don’t hesitate to work through it with a professional.

- Delay your Social Security benefits: If you don’t happen to need any extra funds when you’re of retirement age, you can delay claiming your Social Security benefits. Your benefits will grow by a respectable 8% for every year you delay claiming them between your retirement age and up until you turn 70. This is especially convenient if you have other income sources that can allow you to live comfortably until you start collecting, so make sure to assess how life will pan out for you before taking on this strategy.

- Make Qualified Charitable Distributions (QCDs): As you’ve probably heard before, charitable donations are tax deductible up to 60% on your AGI. Enter qualified charitable distributions (QCDs), which allow you to send money from your IRA straight to the charitable organization of your choice once you turn 70 ½. So, instead of taking an RMD and getting a bigger tax bite, the donation won’t be considered taxable income and you won’t be taxed on the amount. It’s a win-win!

Social Security Benefits And Taxes: FAQ

1. Is social security taxed after age 70?

Yes. A portion of your social security benefits will still be taxable if your income goes above a certain threshold regardless of your age. The regular amount is 50%, but it can go up to 85% for people in higher income brackets.

2. What is my “combined income” (AKA provisional income)?

Combined income is what the IRS uses to determine if you will be taxed on your Social Security benefits, and is the sum of your AGI, 50% of your benefits, and any tax-exempt interest you have.

If the resulting number is between certain amounts (and depending on your filing status), your benefits may be taxable by 50% or 85%.

3. Will I be taxed if Social Security benefits are my only source of income?

Since your taxes will still be based on your income, having Social Security benefits as your only source means you will most likely not be taxed on them.

But, if you add other income sources to that and the total grows past a certain threshold, then you will be taxed on them, along with the rest of your income.

4. Does working past the age of retirement affect Social Security taxation?

Yes, but sadly for the worse. Working past your retirement age means that the additional income you earn can increase your provisional income, so you run the risk of having a bigger portion of your benefits taxed by the IRS.

5. Can I at least lower the taxes of my Social Security benefits?

You actually can, and there are plenty of ways to do so. Some of these options include making early withdrawals from tax-deferred retirement accounts to lower RMDs in the future, delaying your benefits to minimize the taxable portion of your income (and boost your benefits by 8% per year delayed, and converting your regular IRA or 401(k) account into a Roth IRA.

Nick Charveron

Nick Charveron is a licensed tax practitioner and Partner & Co-Founder of Community Tax, LLC. As an Enrolled Agent, the highest tax credential issued by the U.S. Department of Treasury, Nick has unrestricted practice rights before the IRS. He earned his Bachelor of Science from Southern Illinois University while serving with the U.S. Army Illinois National Guard and interning at the U.S. Embassy in Warsaw, Poland. Based in Chicago, Nick combines his passion for finance and real estate with expertise in tax and accounting to help clients navigate complex financial challenges.

Puede que también le guste