Key Takeaways

- Failure to file your taxes will have you penalized by the IRS. The penalties can be fines, liens, and seizure of your property.

- On top of that, the IRS also charges interest on penalties, which can add to a big chunk of change over time.

- Not filing your taxes doesn’t immediately constitute tax evasion, but if you let the situation escalate long enough, the IRS can take you to court eventually.

- The IRS offers plenty of opportunities to properly file and pay back taxes in the form of payment plans and other options.

- Not owing taxes does not exempt you from filing a tax return if your income exceeds a (very low) threshold set by the IRS.

Failure to file your taxes, or filing them late even if you get a tax extension, can bring about bothersome and potentially serious consequences for you, from hefty fines to severe legal troubles depending on the amount owed and how long you haven’t paid them.

That much you probably know already, but there are always related questions around the topic such as: Can you go to jail for not filing taxes? How much is the penalty for not filing your taxes? What if you can’t pay your taxes?

Breaking news: It’s bad for you to not file your taxes. Also, water is wet and the sky is blue. It might seem painfully obvious to state that failure to file or e-file your taxes has some pretty bad consequences, but it’s necessary to part from there so we can go over exactly what happens.

How long will it take for the IRS to notice and take action? What’s the difference between not filing and not being able to pay? And finally, what can you do to avoid all of these situations?

What Happens If You Don’t File Your Taxes

It’s important to differentiate between the different scenarios that can occur. It’s a different conversation with its own set of consequences to file your taxes and fail to pay them, but right now we will focus on what happens if you don’t even file your taxes at all in the first place.

Both scenarios are even contemplated by the IRS in their respective penalties: The Failure to Pay Penalty, and the Failure to File Penalty.

Let’s get it out of the way: It’s better for you in the long run to file your taxes even if you know you can’t pay them. For starters, filing your taxes before the deadline will let you avoid the Failure To File penalty we mentioned.

At least file for an extension if you’re strapped for both cash and time. An extension will give you until October 15 to complete your return and prevent the IRS from piling on the penalties for not filing your taxes on time.

The Penalties For Not Filing Taxes

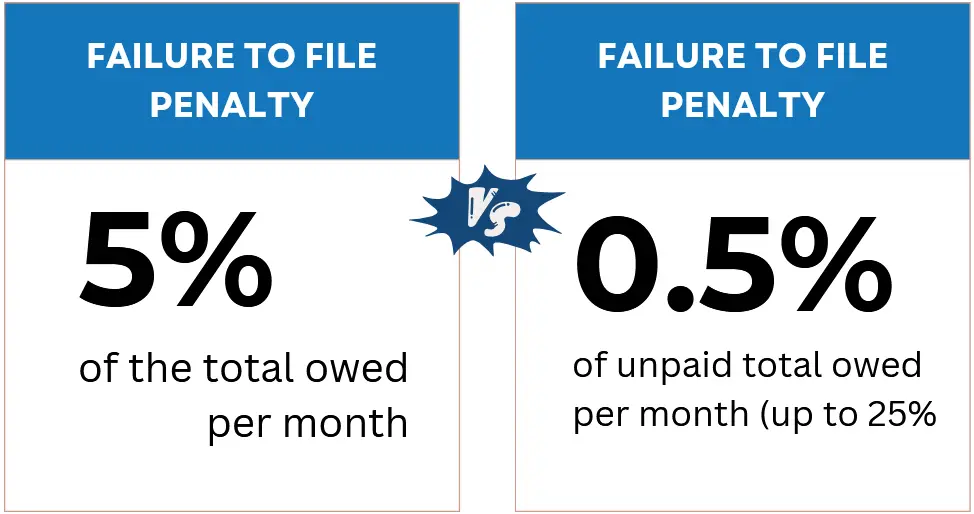

The first thing the IRS will do if you don’t file your taxes is imposing a failure to file penalty, which is 5% of your unpaid tax balance. An additional 5% will stack each month after that up to a maximum of 25% of what you owe after five months have passed.

It follows that if you’re not filing your taxes, you probably aren’t paying them either, so the IRS will move on to a failure to pay penalty, which is 0.5% of your unpaid taxes for each month you don’t pay; this penalty also won’t exceed 25% of your tax liability.

Interest On Penalties

It should come as no surprise that the IRS charges interest on penalties. The interest for the failure to file penalties are due on the return date, and the failure to pay penalties are due on the date you’re notified (or when the penalty is assessed).

Therefore, you won’t be charged interest if you pay the amount owed on or before the “pay by” date that appears on your notice.

Federal Tax Liens And Levies

Whether you don’t file or pay your taxes, letting the problem go on too long will lead you to face federal tax liens or levies. Let’s go over each of them.

A federal tax lien is an official warning issued by the U.S. federal government, essentially a statement of intent about seizing your property in lieu of payment for your taxes.

Since the lien is part of public record, financial institutions will be able to see it and may refuse to provide their services to you because of it.

A federal tax levy is more complicated since it involves the actual seizure of your property — both personal and real — to pay for your tax debt, and it can happen whether you fail to pay your taxes or if you default on a payment plan.

It’s possible to issue a lien and a levy at the same time. Some types of personal property are considered exempt from being levied, as well as some of your major assets depending on the amount owed to the IRS.

How Long Until The IRS Can Seize Your Funds

Once the levy on your property is issued and you have been notified, you have 30 days to respond before the levy goes into effect.

In case the levy is targeting the funds in your bank account, the bank will freeze those funds and hold them for a period of 21 days; after the period is over, those funds will be transferred to the IRS to pay your outstanding tax balance.

While all of these are serious (and are supposed to sound serious), the main thing you should take away from this explanation is that a failure to file your tax returns will most likely lead to penalties, but not jail time (at least not in most cases).

There is a different set of circumstances and actions surrounding the failure to pay taxes that can lead to criminal investigations that could, eventually, land someone in jail, but they’re not really what we’re going for with this guide.

IRS Payment Plans

Next thing you will definitely want to do is to start paying your taxes in monthly installments instead of a lump sum during Tax Day. Here are the most common payment plans contemplated by the IRS:

- One Time Payment: The payment is done either by debit or credit card. This one-time payment option is probably only good if you somehow know you’re going to get enough money to cover your tax liability at a later time than Tax Day.

- Short-Term Payment Plan (180 days or less): Perhaps the most convenient payment plan devised by the IRS, the short-term plan has no set up fees and you can pay through check, money order, debit or credit card (fees do apply to card payments), or directly from your bank account using Direct Pay.

- Long-Term Payment Plan (180 days or more): Because of the extended period of time afforded to you, this plan has a couple of potential fees in order to set it up. The set-up fee is $31 if you use direct debit (which can get waived for low income taxpayers) and a whopping $130 if you don’t use direct debit.

To set up a payment plan, you have to go through the online payment agreement application or by filing Form 9465. You can also call the IRS or even visit their offices to get guidance on how to set up the plan. Keep in mind that if you owe more than $50,000, the terms of your payment plan will be different.

Is Not Filing Taxes The Same As Tax Evasion?

Tax Evasion Vs. Tax Avoidance

Both of these terms, although often used interchangeably, are actually very different concepts, and both are considered as separate things (with only one of them actually being a violation).

Tax avoidance is defined as “an action taken to lessen tax liability and maximize after-tax income”; while the word avoidance makes it sound a little sketchy, the IRS still considers it perfectly legal.

It does make sense if you think about it, as almost any taxpayer is eligible to claim deductions, credits, and other adjustments to make them pay less and get more refunded.

On the other hand, tax evasion— which is defined as the failure to pay or a deliberate underpayment of taxes — is illegal, plain and simple.

The most common way that people evade taxes is underreporting their total income for the year, particularly when the money comes from non-traditional sources such as illegal activities and the underground economy.

Common Misconceptions About Not Filing Taxes

There are many myths and misconceptions surrounding the failure to file your tax returns on time. Here are some of the most common ones and the reasons why you should stop believing them if you want to stay out of trouble with the IRS.

If You Don’t Owe Taxes You Don’t Have To File

Wrong! As we described before, filing a tax return is mandatory even for taxpayers who technically owe nothing to the IRS, provided that their income is above a certain threshold (which is quite low, don’t get your hopes up).

By choosing not to file a return because you don’t owe taxes is just opening yourself up to penalties and other legal consequences down the line.

On top of that, by not filing a return during tax season means you’re missing out on refunds or credits that you probably qualify for, such as the Earned Income Tax Credit (EITC).

You Don’t Have To File If You Don’t Make Money

It’s a very common misconception that people with low or no income are exempt from filing taxes.

As mentioned in the previous section, there are income thresholds that do exempt some individuals, but employee wages are far from the only type of taxable income; for example, making even $400 or more from self-employment obligates you to file and pay taxes on those earnings.

The IRS Hasn’t Contacted Me So I Just Don’t File

Big mistake. Just because the IRS hasn’t sent an audit request doesn’t mean you’re not on their radar. The IRS relies on plenty of tools other than self-reporting to track your income.

Employers also file Forms W-2 and 1099, and financial institutions can submit account activity, both of which can be used to catch up with you. So, the IRS not contacting you doesn’t put you in the clear; on the contrary, it will only increase penalties once they do.

I Haven’t Filed Taxes In Years, So I’m Too Far Behind To Catch Up

While it’s true that paying back taxes is an intimidating prospect (particularly if you’ve neglected them for years), the fact is that ignoring them is only delaying the inevitable as there is no statute of limitations to speak of when it comes to back taxes.

Instead, it’s preferable to take the chance offered by the IRS to file late tax returns, as catching up (slow as it may be) may reduce your penalties or avoid them completely in some cases. Along with payment plans, this is a good way to minimize the consequences of a bad track record with taxes.

What Happens If You Don’t File Taxes: FAQ

1. Can the IRS file my tax return for me?

The IRS can actually file a return for you through a form called Substitute For Return. This document will only include the income reported by your employers, and will not allow for deductions, credits or exemptions in your favor. Also, the substitute for return will carry a late-filing penalty, so all in all, it’s definitely not a good replacement for filing your own tax return.

2. Can I go to jail for not filing my tax return?

The truth is that it depends on multiple factors. While failing to file a tax return is a misdemeanor, the IRS would have to prove that an overt, willful act of tax evasion has occurred in order to elevate the situation to a felony, which would then be grounds for a jail sentence if the taxpayer is found guilty (which, honestly, is the likeliest scenario). That being said, the IRS usually only doles out civil penalties to most people, followed by numerous warnings and plenty of chances to file even years after the first offense.

3. Can I file my own return after the IRS files a return for me?

Yes, you can file a past-due return of your own over the substitute for return issued by the IRS through an “SFR reconsideration. You will still have to pay the “failure to file” penalty, but filing your own return allows you to claim exemptions, credits and adjustments, while the SFR does not.

4. Is there a statute of limitations on late tax returns?

Unfortunately no, there is no such thing as a statute of limitations on unfiled tax returns. No matter when it happened, the IRS can go back to any year that you didn’t file your taxes and issue penalties based on your tax liability that year. Still, the IRS doesn’t usually allow for unfiled tax returns to become older than six years in order to enforce actions against taxpayers, and they can even freeze your latest filed return until you file and pay the one you owe.

5. When is my tax return considered “late”?

Any individual tax return postmarked after midnight on Tax Day (which is April 15), although the date can be pushed back to the next business day in case April 15th falls on the weekend. Also, if you mail your return, they will be considered filed on the day they were filed and not when the IRS receives them, but remember that the post office no longer stays open until midnight on Tax Day. People living outside the U.S. automatically get a two-month filing extension.

Jacob Dayan

Entrepreneur • CEO Community Tax, LLC

Jacob Dayan is the CEO and co-founder of Community Tax LLC, a leading tax resolution company known for its exceptional customer service and industry recognition. With a Bachelor’s degree in Business Administration from the University of Michigan’s Ross School of Business, Jacob began his career as a financial analyst and trader at Bear Stearns and Millennium Partners before transitioning to entrepreneurship. Since 2010, he has led Community Tax, assembling a team of skilled attorneys, CPAs, and enrolled agents to assist individuals and businesses with tax resolution, preparation, bookkeeping, and accounting. A licensed attorney in Illinois and Magna Cum Laude graduate of Mitchell Hamline School of Law, Jacob is dedicated to helping clients navigate complex financial and legal challenges.