1 or 0? But the answer is, there’s an art to doing your taxes.

If you are a single parent with one child and are trying to determine how many allowances to claim on your W-4 form, the answer will depend on your specific financial situation. Typically, for a single person with one job, claiming 1 or 2 allowances is standard.

If you have multiple jobs or other sources of income, you may want to adjust your allowances accordingly to avoid underpayment penalties at tax time. It’s important to note that claiming too many allowances may result in owing more money at tax time, while claiming too few may result in a larger tax refund but less money in each paycheck.

To determine the appropriate number of allowances for your individual situation, it may be helpful to use a W-4 calculator or consult with a tax professional. Ultimately, the goal is to accurately withhold the correct amount of federal income tax from your monthly paychecks based on your personal circumstances.

Understanding the W-4 Tax Form

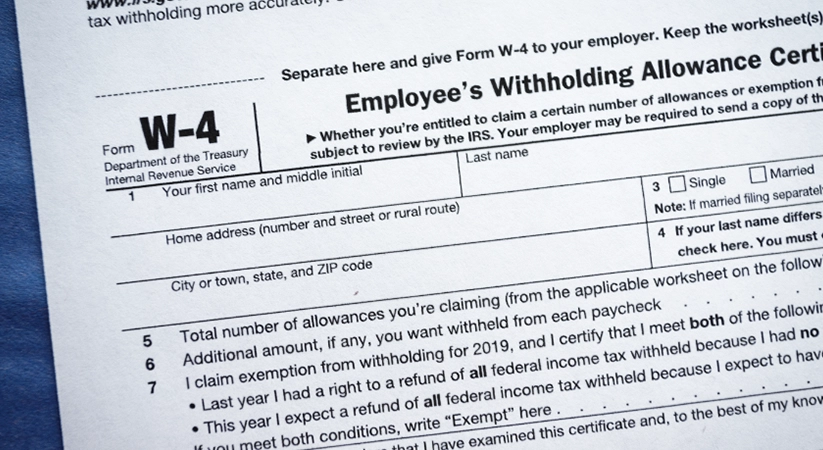

The W-4 form, also known as the Employee’s Withholding Certificate, is a document that instructs your employer on how much money to withhold from your paycheck for federal taxes. It is a crucial form that helps determine the amount of taxes you owe and can affect the size of your paycheck. Understanding the W-4 can be challenging, but taking the time to fill it out correctly can save you from unexpected tax bills or penalties at tax season.

Overview of Allowances and the W-4

The W-4 form is a document that employees complete when starting a new job or when they wish to adjust their federal income tax withholding. Allowances are a way of telling your employer how much federal income tax to withhold from your paycheck. The number of allowances claimed will impact the amount of taxes withheld from your paycheck and the size of your tax refund. A higher number of allowances generally means less tax withheld and a smaller tax refund, while claiming fewer allowances results in more taxes withheld and a larger refund. It’s important to periodically review your allowances and make adjustments as needed to ensure you’re not overpaying or underpaying your taxes. Ultimately, the number of allowances you claim will depend on your personal financial situation. What’s your filing status? Where’s income coming from? How much is it? Utilizing a W-4 calculator or speaking with a tax professional can help you determine the right number of allowances to claim.

The Number of Allowances Meaning?

The number of allowances you claim on your W-4 form directly affects how much income tax is withheld from your paycheck by your employer. The more allowances, the less tax withheld. Conversely, claiming fewer allowances will increase the amount of tax withheld from your paycheck.

The number of allowances you can claim depends on various factors such as your filing status, expected taxable income, number of dependents, and eligibility for tax credits. For instance, if you are a single individual with one child and you are the sole provider, you can claim two allowances on your W-4 form – one for yourself and another for your child.

It is important to note that the number of allowances you claim must be accurate to avoid owing the IRS money or receiving a smaller refund than anticipated. For example, claiming too many allowances may result in owing more taxes at the end of the year, while claiming too few allowances may lead to a larger refund but less money in your paycheck each month.

It Seems Binary: What’s the Difference Between Claiming 1 and 0?

When filling out your W-4 form, you may notice that you have the option to claim either 1 or 0 allowances. But what exactly does this mean, and how does it affect your federal income tax withholding? The number of allowances you claim determines the amount of federal income tax that is withheld from your paycheck, so it’s important to understand the difference between claiming 1 and 0.

Claiming 1 on Your Taxes

Claiming 1 on your taxes could be beneficial for individuals who are single with one child. By doing so, the amount of taxes withheld from each paycheck is reduced, leading to a larger paycheck instead of waiting for a tax refund. This can be helpful for those who have immediate financial needs and cannot wait until tax season for a refund. Additionally, claiming 1 may also result in less underpayment penalties if you end up owing taxes at the end of the year.

It’s important to keep in mind that choosing to claim 1 or 0 on a W-4 form depends on individual financial situations. While claiming 1 can result in a larger paycheck each pay period, it may also result in owing taxes at the end of the year. Therefore, it’s essential to understand your tax situation and make an informed decision.

Claiming 0 on Your Taxes

When it comes to taxes, many people are unsure about how many allowances they should claim. Claiming 0 can be beneficial for those who want the largest amount withheld from their paycheck. This can result in a larger refund check when tax season comes around.

Claiming 0 is often recommended for individuals who have parents that are claiming them as a dependent on their taxes. It can also be helpful for those who have other sources of income that may push them into a higher tax bracket. By claiming 0, the maximum amount of taxes is withheld from each paycheck, decreasing the likelihood of owing money at tax time.

Furthermore, a larger refund check can help cover expenses such as bills, vacations, or loans. It’s important to note that claiming 0 may result in a smaller paycheck each pay period. However, this sacrifice can lead to a larger refund check and provide financial relief in the long run.

I’m Married. So Should I Put 0 or 1 on My Form W-4?

Deciding whether to claim 0 or 1 when filling out your W-4 form as a married person requires considering several factors. If both you and your spouse have jobs and are in the same income bracket, claiming 0 could result in more taxes being withheld from your paychecks than necessary.

This could leave you with a smaller paycheck each pay period and a larger refund at the end of the year.

However, claiming 1 could result in underpayment and a potential tax bill at the end of the year if both spouses earn equal incomes or if one spouse has a significantly higher income. In this case, opting for additional withholding, such as filling out form W-4 line 6 or requesting additional withholding on your pay stub, can ensure you are paying enough taxes throughout the year.

Ultimately, your decision should be based on your personal tax situation and goals.

Claiming 0 or 1 affects your tax payments and refunds differently, and it is important to consider both to make the best decision for your financial situation as a married couple.

Calculating Your Allowances

When it comes to filling out a W-4 form and determining how many allowances you should claim, it can be overwhelming and confusing. The number of allowances you claim affects the amount of federal income tax withheld from your paycheck, ultimately determining the amount of your tax refund or tax bill. Claiming more allowances means less tax is withheld, resulting in more money in your paycheck but a potentially smaller tax refund or even owing taxes at the end of the year. On the other hand, claiming fewer allowances means more tax is withheld, resulting in a larger tax refund but less money in your paycheck.

Standard Deduction vs. Itemized Deduction

When filing your taxes, you have two options for deductions: standard or itemized. The standard deduction is a fixed dollar amount that reduces your taxable income, while an itemized deduction is a list of eligible expenses that you can subtract from your income.

The decision to choose between the two depends on your specific situation. If your eligible itemized deductions exceed the standard deduction amount, then itemizing is the better choice. Examples of itemized deductions include mortgage interest, property taxes, medical expenses, and charitable donations. On the other hand, if your eligible itemized deductions are lower than the standard deduction amount, then taking the standard deduction is a more beneficial option.

It’s important to consider your personal situation and the potential tax benefits before deciding which deduction to choose. In some cases, seeking out the advice of a tax professional can be helpful.

Personal Exemptions and Dependents

To properly list the number of children or dependents in Step 3 of the W-4 form, enter the total number you have, including children, other dependents, and the spouse whom you will claim as a dependent on your tax return.

To calculate the number of allowances to claim based on personal exemptions and dependents, use the IRS’s withholding calculator or refer to the instructions on the W-4 form. Keep in mind that claiming too few allowances may result in underpaying taxes and owing money at tax time, while claiming too many allowances could lead to overpaying and receiving a smaller tax refund. It’s important to find a balance that suits your individual financial situation.

Making Adjustments to Your Withholdings

Making adjustments to your withholdings is an important step towards managing your finances, especially during tax season. It involves determining how much of your income should be withheld by your employer for federal income tax purposes. This can depend on various factors such as your filing status, taxable income, and other personal circumstances, which are declared on the W-4 form. If your financial situation changes throughout the year, it’s advisable to review your tax withholdings and make necessary adjustments to avoid underpayment penalties when it’s time to file your tax returns. In this article, we will discuss the importance of tax allowances, the difference between claiming 1 or 0 allowances, and how to use a W-4 calculator to determine the right amount of withholdings for your personal situation.

Adjusting for Tax Season Refunds or Large Tax Bills

Adjusting your tax withholdings is essential to avoid underpayment penalties or getting hit with a large tax bill. To make the best adjustment to your withholdings, consider your personal situation, like any changes to your income, marital/filing status, or deductions. Start by estimating your taxable income and calculating your expected tax liability. This will give you an idea of the difference between your expected tax bill and what you’ve prepaid in withholdings.

If you’re not sure how to adjust your withholdings, a tax professional can guide you through the process. Alternatively, you can use a W-4 calculator, available online, that will ask you a series of questions about your income and expenses to help determine the right amount to withhold. Remember that getting a larger tax refund may seem nice, but it means you’ve given the government an interest-free loan during the year. Adjusting your withholdings can help you keep more of your money throughout the year and avoid unwanted surprises come tax season.

Additional Withholding Options for Unexpected Income Changes

When unexpected income changes happen, it’s important to adjust your withholding to avoid underpayment penalties or a large tax bill at the end of the year. Fortunately, there are additional options available to adjust your withholding beyond just filing a new W-4 form.

The IRS offers an online Withholding Calculator that can help you determine the correct amount of withholding based on your tax situation and income. It’s especially helpful when you experience changes in income or life circumstances, such as getting married or having a child.

Form W-4P is another option you can use if you receive retirement income or other forms of income that do not have taxes withheld. By filling out this form, you can adjust the amount of taxes withheld from these types of income.

Both the Withholding Calculator and Form W-4P are free and easy to use. They provide step-by-step instructions and are designed to help you adjust your withholdings accurately and efficiently. Use them when unexpected income changes occur to ensure that your tax returns and withholdings are aligned with your financial situation.

Jacob Dayan

Entrepreneur • CEO Community Tax, LLC

Jacob Dayan is the CEO and co-founder of Community Tax LLC, a leading tax resolution company known for its exceptional customer service and industry recognition. With a Bachelor’s degree in Business Administration from the University of Michigan’s Ross School of Business, Jacob began his career as a financial analyst and trader at Bear Stearns and Millennium Partners before transitioning to entrepreneurship. Since 2010, he has led Community Tax, assembling a team of skilled attorneys, CPAs, and enrolled agents to assist individuals and businesses with tax resolution, preparation, bookkeeping, and accounting. A licensed attorney in Illinois and Magna Cum Laude graduate of Mitchell Hamline School of Law, Jacob is dedicated to helping clients navigate complex financial and legal challenges.