Top 5 Most Popular Itemized Deductions for U.S. Taxpayers

Published:

Key Takeaways

- It’s Not For Everyone: Itemizing your tax deductions makes sense if your total deductible expenses exceed the standard deduction. If your itemized deductions don’t add up to more than the standard deduction, then it’s just not worth it to itemize your deductions—stick with the standard deduction as it saves time and paperwork.

- The Range Of Expenses: Itemized deductions cover medical expenses, charitable donations, casualty losses from federally declared disasters, and more. The key is knowing what’s eligible and keeping good records.

- Medical Expenses Threshold: When deducting medical expenses, you can only deduct medical expenses that exceed 7.5% of your adjusted gross income (AGI). So, if your AGI is $50,000, only expenses over $3,750 are deductible. This threshold means that small medical bills won’t make a dent, but if you had a major health event or large out-of-pocket costs, it could add up.

- State and Local Taxes (SALT) Cap: You can deduct state and local income, sales, and property taxes, but the SALT deduction is capped at $10,000 ($5,000 if married filing separately). Before itemizing, be sure to check how much SALT you’ve paid to see if it’s worth it, especially if you live in a state with high taxes.

- Proper Documentation Is Key: You know the IRS loves their receipts. To claim itemized deductions, keep detailed records like receipts, bank statements, etc. For things like medical expenses, detailed bills showing dates of service and payments are a must. Pretty much everything you can think of!

Itemizing your tax deductions can decrease your taxable income by a sizable amount, but you can’t just choose whatever expenses that catch your fancy. Familiarize yourself with how itemized deductions work and avoid the IRS’ wrath!

Itemized Tax Deductions: A Guide to Maximizing Your Savings

When filing your income tax return, certain expenses qualify as deductions, often referred to as itemized deductions. While many taxpayers default to the standard deduction for simplicity, understanding itemized deductions can potentially save you more money. Here’s what you need to know to make an informed decision.

When Should You Consider Itemizing?

As you might imagine, itemizing is available to everyone, but it’s not really for everyone. You should consider doing so only if the total amount of your eligible expenses exceeds the standard deduction for your filing status.

The IRS allows taxpayers to choose between taking the standard deduction or itemizing them individually, and the goal is to lower your taxable income as much as possible.

Here are some situations where itemizing might make sense:

- You Have Large Medical Expenses:If your unreimbursed medical and dental expenses exceed a certain percentage of your adjusted gross income (AGI), you may benefit from itemizing.

- You Paid a Lot in State and Local Taxes (SALT): You can deduct state and local income (or sales) taxes, plus property taxes, up to a combined total of $10,000 ($5,000 if married filing separately).

- You Have Significant Mortgage Interest: If you have a mortgage, the interest paid on it may be deductible. This is especially beneficial if you recently bought a home and are paying mostly interest.

- You Made Large Charitable Contributions: Donations to qualified charities can be deducted, making itemizing worthwhile if you contribute generously.

- You Have Other Miscellaneous Deductions: Some job-related expenses and investment expenses may also be deductible, but the rules on these have changed in recent years.

In the end, you should compare your total itemized deductions with the standard deduction to determine which option will save you the most money—this takes some time and effort, but having a clear idea of where your finances stand is always better.

If you don’t trust your math chops, using tax software or hiring a tax professional can help you crunch the numbers.

Regulations About Itemized Deductions to Keep in Mind

Itemized deductions are subject to a variety of IRS rules, including eligibility criteria, deduction limits, and documentation requirements. Here are some key regulations to keep in mind:

- Medical Expenses: Only medical and dental expenses that exceed 7.5% of your AGI are deductible.

- State and Local Taxes (SALT Cap): You can deduct state and local income, sales, and property taxes, but the total deduction is capped at $10,000 ($5,000 for married filing separately).

- Mortgage Interest: Interest on mortgages up to $750,000 (or $1 million for older loans) is deductible. Home equity loan interest is only deductible if used for home improvements.

- Charitable Contributions: Generally, donations are deductible up to 60% of your AGI, but different limits may apply depending on the type of donation and the organization.

- Casualty and Theft Losses: These are only deductible if they occur in a federally declared disaster area.

- Miscellaneous Deductions: Many work-related and investment expenses were eliminated under the Tax Cuts and Jobs Act, but some still apply for specific professions or self-employed individuals.

Additionally, the IRS requires you to keep detailed records of your deductions, such as receipts, bank statements, and proof of payment. If you’re audited, you’ll need to provide documentation to support your claims.

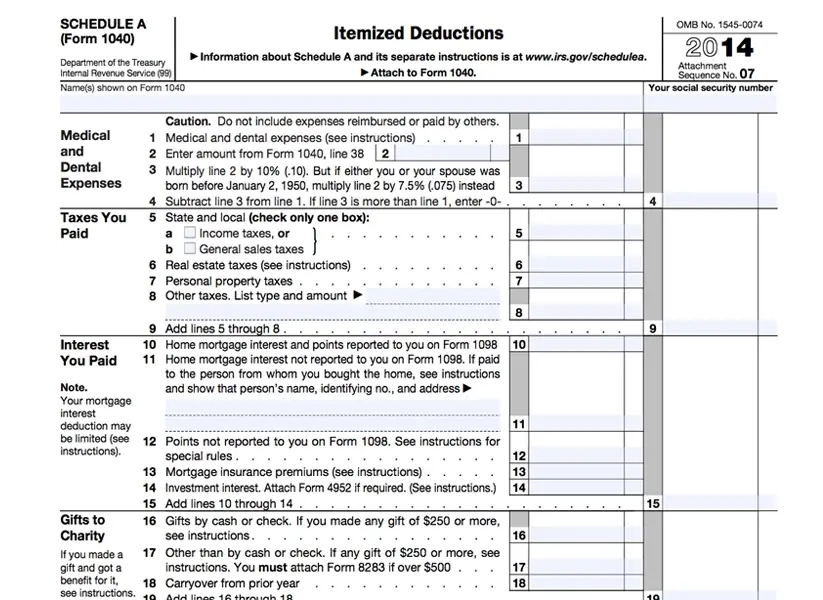

The 5 Most Popular Itemized Tax Deductions

1. Mortgage Interest

Homeowners can deduct interest paid on mortgages for their primary residence (and sometimes a second home), up to a certain loan limit. This is one of the biggest deductions for many taxpayers.

2. State and Local Taxes (SALT)

You can deduct state income, sales, and property taxes, but remember the $10,000 cap. This deduction is particularly valuable in high-tax states.

3. Charitable Contributions

Donations to qualified charities are deductible if you have proper documentation. This includes cash donations and the fair market value of donated goods.

4. Medical and Dental Expenses

Deductible if they exceed 7.5% of your AGI. Eligible expenses include surgeries, prescription medications, dental treatments, and even some travel costs for medical care.

5. Investment Interest Expense

If you borrowed money to invest (like on margin), you can deduct the interest paid on that loan, up to the amount of your net investment income.

These are just a few examples; many other expenses may qualify depending on your financial situation.

Who Is Required to Itemize Deductions?

Nobody is ever required to itemize deductions—it’s always a choice. Sometimes, however, there are situations where itemizing is the only option you have. If you’re ever in any of these tax situations, you’re not allowed to take the standard deduction, and will have to itemize them instead:

Married Individuals Filing Separately (Certain Cases)

If one spouse itemizes, the other cannot take the standard deduction and must also itemize.

Nonresident Aliens and Certain Other Taxpayers

Standard deductions aren’t available for nonresident aliens, dual-status aliens, and individuals filing returns for short tax years. These taxpayers may need to itemize to claim deductions.

Still, for most people, itemizing deductions is a decision based on financial benefit rather than a requirement. If your itemized deductions don’t exceed the standard deduction, taking the standard deduction is usually the better choice.

The Final Word on Itemized Deductions

When it comes to deductions on your tax return, knowing is truly half the battle. The better you understand itemized tax deductions, the easier it will be to file your income tax return accurately and efficiently.

It’s not just a question of identifying all possible deductions so you can minimize your taxable income; it’s also about being able to provide evidence about it and learning if a possible deduction applies to your specific tax situation.

Take the time to evaluate your financial situation annually—it could lead to substantial savings.

Understanding Itemized Tax Deductions: FAQ

- What are itemized deductions?

Itemized deductions are specific expenses that the IRS allows you to subtract from your taxable income, reducing your overall tax bill. Instead of taking a flat standard deduction, you list each deductible expense individually on Schedule A of your tax return. - When should I itemize instead of taking the standard deduction?

You should consider itemizing if your total deductions exceed the standard deduction amount. This often applies to people with significant mortgage interest, large charitable contributions, high medical expenses, or substantial state and local taxes. - Can I itemize deductions if I’m married but filing separately?

Yes, but there’s a catch: if one spouse itemizes, the other must itemize as well, even if their deductions are less than the standard deduction. This rule ensures both spouses are consistent, which can be a disadvantage if one has few deductible expenses. - Are there deductions I can’t itemize?

Absolutely. Personal expenses like groceries, rent, and commuting costs are not deductible. Also, unreimbursed employee expenses are mostly off the table due to changes from the 2017 tax reform, unless you fall into specific categories like armed forces reservists or qualified performing artists. - Can I itemize deductions if I don’t own a home?

Yes! While homeowners often benefit from itemizing due to mortgage interest deductions, renters can still itemize if they have significant medical expenses, charitable donations, or other qualifying deductions that surpass the standard deduction. - Do itemized deductions reduce my taxable income dollar-for-dollar?

Yes, itemized deductions reduce your taxable income directly. For example, if you earn $80,000 and have $15,000 in itemized deductions, your taxable income becomes $65,000. This reduction can lower the amount of tax you owe significantly. - What happens if I make a mistake on my itemized deductions?

If you realize you made an error after filing, you can file an amended return using Form 1040-X. If the IRS catches the mistake, they might send you a notice to correct it, and depending on the error, it could result in additional taxes owed, penalties, or interest. Accurate documentation helps prevent mistakes.

Related Articles

You May Also Like