There’s an alternative to regular taxes? Yeah, paying more.

Alternative minimum tax (AMT) is a tax system implemented in the United States to ensure that high-income taxpayers cannot use tax deductions and credits to lower their taxes too much. The AMT system is designed to calculate taxes owed by taking into account all types of income, including those that are exempt from regular tax rules. It is a measure of income that goes beyond regular taxable income as defined by the Internal Revenue Service (IRS).

Who does AMT apply to?

The Alternative Minimum Tax (AMT) was originally created to target a small percentage of high-income taxpayers who were able to use various tax breaks and deductions to significantly reduce their tax liability. However, due to the lack of indexing for inflation, the AMT has increasingly affected a larger group of middle-income taxpayers in recent years.

Although the AMT applies to a wider range of taxpayers than originally intended, it is still important to note that most taxpayers do not need to worry about this tax. An exemption amount applies and only begins to phase out once an individual reaches a certain income level.

Certain types of income, such as incentive stock options and foreign tax credit, and deductions subject to certain limits, such as state and local taxes and medical expenses, can also cause the AMT to apply.

How does the alternative minimum tax (AMT) system work?

Alternative minimum tax (AMT) is a tax system that is designed to ensure that high-income taxpayers with various deductions and credits are not able to avoid paying their fair share of taxes. If you fall into this category, then AMT can significantly impact your tax liability. To calculate AMT, the IRS requires taxpayers to perform a separate calculation using a different set of rules than those used to calculate regular income tax liability. Whichever calculation results in a higher tax liability is the amount you must pay. Several factors can trigger AMT, such as high household income, capital gains, and even exercising incentive stock options (ISOs). If you’re a high-income earner or own a considerable amount of investments, there’s a chance that you might have to pay AMT.

To determine whether you owe AMT or not, it’s essential to compare your regular tax liability to your AMT liability.

If your AMT liability is higher, then you must pay the difference. Conversely, if your regular tax liability is higher, then you don’t need to worry about AMT.

AMT Calculation Process

The AMT calculation process involves adding back certain deductions and exclusions that are allowed under regular tax rules to calculate taxable income. Taxpayers also need to determine whether they have any alternative minimum tax preferences or adjustments that are unique to the AMT system. These adjustments could include incentive stock options, tax-exempt interest, certain foreign tax credits, and other tax benefits.

Once you have determined your alternative minimum taxable income, you need to apply the applicable tax rate to calculate your tentative minimum tax. This tax is then compared to your regular income tax liability, and whichever amount is higher is the one you must pay.

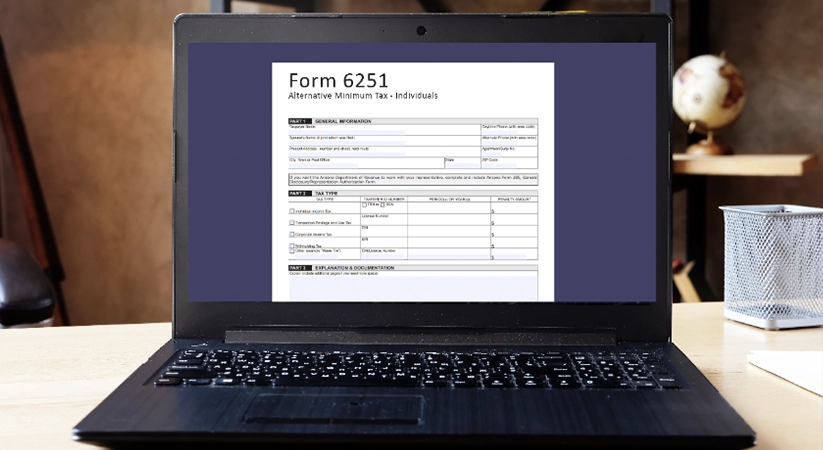

Understanding IRS Form 6251

The IRS Form 6251 is the form that taxpayers must use to calculate and report their alternative minimum tax liability. This form requires you to add back a variety of deductions that are allowed under regular tax rules, including state and local taxes, medical expenses, and miscellaneous itemized deductions.

There are also certain income sources that may be tax-free under the normal income tax system but need to be included when calculating AMT, such as tax-exempt interest, and other types of income that receive preferential treatment.

AMT Exemption

The AMT exemption is a provision that can reduce the amount of alternative minimum tax that a taxpayer owes. This exemption is similar in concept to the standard deduction or personal exemption that is used in the regular tax system. The exemption amount varies based on your filing status.

When you are calculating your tentative minimum tax, you can subtract the AMT exemption amount to determine your final AMT tax liability. You don’t owe any if your regular tax liability is more.

Types of Income Affected by the AMT

The alternative minimum tax (AMT) is designed to ensure that wealthy people and high-income earners pay their fair share of taxes. One way that the AMT system does this is by including certain types of income that receive preferential treatment under normal income tax rules.

Earned Income

High household income or earned income refers to what a taxpayer receives from salaries, wages, tips, and other taxable forms of pay.

The AMT is a separate tax system with its own set of rules. It was designed to ensure that high-income taxpayers are not able to avoid paying their fair share of taxes by taking advantage of common tax breaks and deductions. When calculating AMT, income adjustments such as personal exemptions and state and local taxes are included, which can reduce or eliminate certain tax breaks.

For taxpayers with high earned income, the AMT may limit their ability to take advantage of common tax breaks, such as the standard deduction and exemption amounts. This can increase the taxpayer’s overall tax liability and complicate tax calculations.

Interest Income

Interest income can be affected by the alternative minimum tax (AMT), which is a separate tax system that operates alongside the regular tax rules. The AMT was designed to ensure that high-income taxpayers pay their fair share of taxes by preventing them from taking advantage of common tax breaks and deductions. Interest income is subject to AMT, and the rules for calculating this tax are different from those used in the regular tax system.

In the regular tax system, interest income is generally taxed at the taxpayer’s ordinary income tax rate. However, in the AMT system, certain types of interest income may be subject to a higher tax rate. For example, tax-exempt interest on private activity bonds and certain other types of municipal bonds can be subject to AMT. This is because these bonds are often used to fund projects that provide significant tax benefits, such as low-income housing, which the government wants to encourage. As a result, the government has chosen to require taxpayers to pay AMT on the interest income from these bonds.

In addition to these specific rules regarding interest income, the AMT system includes a broader set of rules called “tax preference items,” which are designed to limit the amount of tax breaks and deductions that high-income taxpayers can claim. Tax preference items include things like incentive stock options, certain kinds of deductions, and other types of income. These items reduce the amount of tax owed in the regular tax system but increase the taxpayer’s liability under AMT.

Capital Gains and Dividends

One of the most notable features of the alternative minimum tax (AMT) system is that it can subject certain types of income, including capital gains and dividends, to a higher tax rate than the regular income tax system. Capital gains are the profits earned from the sale of an asset, such as stocks, bonds, or real estate. Meanwhile, dividends are payments made by companies to their shareholders as a distribution of profits.

When calculating AMT, capital gains are treated as positive AMT income, meaning they are added to the taxpayer’s overall income subject to the alternative tax. In contrast, qualified dividends are actually subtracted from the taxpayer’s regular AMT income. This may seem counterintuitive, but it’s designed to ensure that only the portion of dividends that are not taxed at the regular income tax rate are subject to AMT.

It’s important to note that different tax rates apply to capital gains and dividends for regular tax and AMT purposes. Under the regular tax system, capital gains are taxed at varying rates depending on the holding period of the asset, with long-term gains generally taxed at a lower rate. Similarly, dividends are taxed at different rates depending on whether they are classified as qualified or non-qualified.

However, for AMT purposes, capital gains are included in the calculation at a different tax rate than the regular income tax rate. This can result in a higher tax liability for taxpayers with significant gains. On the other hand, qualified dividends are taxed at the same rate for both regular tax and AMT purposes, which provides some relief for taxpayers who rely on dividend income.

Incentive Stock Options (ISOs)

Incentive Stock Options (ISOs) are a common tool used by companies to incentivize and retain employees. These employee stock options provide the right to buy company shares at a predetermined price, also known as the strike price, on or after the grant date. The benefit of ISOs is that they offer tax advantages to the employee when exercised.

The grant date is when the employer offers the ISOs to the employee, and the strike price is the price at which the employee can buy shares when they decide to exercise their options. The number of shares that an employee can purchase is also specified in the grant agreement.

One of the significant advantages of ISOs is the potential for lower capital gains rates when the shares acquired by exercising the options are sold. If the shares are held for more than a year after exercise and two years after the grant date, the difference between the strike price and the fair market value of the shares at exercise is taxed at the lower long-term capital gains rate, instead of the ordinary income tax rate.

Other Categories of Income

There are several additional types of income that may trigger AMT liability, including distributions from certain types of trusts and estates, tax-exempt interest from private activity bonds, and income adjustments related to certain depreciation methods.

Private activity bonds are bonds issued by state and local governments to finance certain types of projects, such as airports and housing developments. The interest earned on these bonds is tax-exempt at the federal level, but it must be added back to taxable income when calculating AMT liability. This means that individuals who receive tax-exempt interest from private activity bonds may face AMT liability if their income exceeds certain phase-out thresholds.

Income adjustments can also play a role in AMT liability. Certain depreciation methods, such as accelerated depreciation, may reduce taxable income under regular tax rules but must be added back to income when calculating AMT liability. This adjustment can significantly increase an individual’s AMT liability, particularly for those with high levels of income.

It’s important to note that there may be phase-out thresholds or other limitations that apply to these forms of income. For example, the phase-out threshold for tax-exempt interest from private activity bonds varies based on filing status and can change from year to year. As such, it’s important to consult with a tax professional or use an AMT calculator to ensure that all relevant forms of income are properly accounted for when calculating AMT liability.

The Right Way to Calculate Your Alternative Minimum Taxes

Calculating AMT liability is crucial because it is different from regular tax liability and can significantly impact your tax burden. AMT liability is the minimum amount of federal income tax that certain taxpayers are required to pay.

The AMT system was designed to prevent high-income taxpayers from using common tax breaks such as deductions subject to “phase-out thresholds” to avoid paying their fair share of federal income taxes. Since the calculation of AMT liability is different from regular tax liability, the taxpayer should evaluate and compare both to determine their actual tax payment.

Here’s How It Works

- Calculate your taxable income, but with fewer tax exclusions and tax deductions, as dictated by the AMT rules on IRS Form 6251.

- Subtract the AMT exemption amount.

- Multiply what’s left by the appropriate AMT tax rates. The AMT has two tax rates: 26% and 28%. IRS Form 6251 has the details.)

- Subtract the AMT foreign tax credit, if you qualify for it. What’s left is your income tax under the AMT rules.

- Check to see if your taxes under AMT rules are higher than under regular rules. That’s how you know who has to pay AMT.

- Pay the higher amount.

AMT exemption amounts for 2023

The AMT exemption amount is the amount of income that an individual can earn before becoming subjected to the AMT system. For the 2023 tax year, the AMT exemption amounts are

- $81,300 for single taxpayers

- $126,500 for married filing jointly

- $63,250 for married couples filing separately

Comparing Regular Tax vs. AMT Liability

While the regular tax system is familiar to most taxpayers and is built on a set of tax brackets with progressively increasing tax rates, the AMT system operates differently with a fixed tax rate and fewer deductions and exemptions. Under the regular tax system, taxpayers are taxed based on their income and corresponding tax rates. The tax rates are progressive, meaning that as income levels increase, the tax rate increases as well. In contrast, the AMT system has a fixed tax rate of 26% for incomes up to $206,100 (for single filers) and 28% for incomes above that threshold.

How do I know if I have to pay alternative minimum tax?

You may have to pay alternative minimum tax if your income exceeds a certain threshold and you have substantial itemized deductions, tax-exempt private activity bonds, or incentive stock options.

High-income taxpayers are most likely to be subject to the AMT if they claim substantial itemized deductions or have significant income from tax-exempt private activity bonds or exercise incentive stock options.

Jacob Dayan

Entrepreneur • CEO Community Tax, LLC

Jacob Dayan is the CEO and co-founder of Community Tax LLC, a leading tax resolution company known for its exceptional customer service and industry recognition. With a Bachelor’s degree in Business Administration from the University of Michigan’s Ross School of Business, Jacob began his career as a financial analyst and trader at Bear Stearns and Millennium Partners before transitioning to entrepreneurship. Since 2010, he has led Community Tax, assembling a team of skilled attorneys, CPAs, and enrolled agents to assist individuals and businesses with tax resolution, preparation, bookkeeping, and accounting. A licensed attorney in Illinois and Magna Cum Laude graduate of Mitchell Hamline School of Law, Jacob is dedicated to helping clients navigate complex financial and legal challenges.