Key Takeaways

- The higher your income is, the higher tax bracket you will fall into, meaning that your taxable income will be taxed at a higher rate; this is a progressive income tax method.

- There are seven marginal tax rates, which are defined by income level.

- Your effective tax rate is the average tax rate you paid on your income, once you’ve paid the tax rate on every tax bracket your income falls into.

- Factors like income level, your filing status, and any applicable deductions, credits and exemptions all affect your final tax rates.

With different brackets, deductions, and credits to consider, it’s easy to feel overwhelmed. But don’t worry, you’ll find everything you need to know inside this handy guide.

The federal income tax system works on a principle that (in paper) is extremely simple: The more you have, the more you owe; in other words, the higher your income is, the higher your taxes on that income will be. To accommodate both high- and low-income people in the same scale, the “tax bracket” was created.

Tax bracket refers to the specific income range where you are and the corresponding tax rate that will apply to you. But what exactly do they work? What factors bring you higher or lower on the income range? And more importantly, just how do you determine what’s your tax bracket?

This guide will answer all of those questions and more, so by the end you’ll have a more complete understanding of tax brackets and how they apply to you. Keep reading and learn more!

How To Know What Tax Rate To Use

As we’ve mentioned already, the U.S. has a progressive tax system, meaning that people with higher incomes are subject to higher federal taxes, and people with lower incomes owe less. That part is simple. The part that’s a little more complicated is making sense of tax brackets and whether they apply to you before or after calculating your taxable income. So, let’s go over some of the finer details.

What Is A Tax Rate?

Tax brackets are simply the categories in which people of different income levels fall into. Think of them as the cutoff values for taxable income, and the higher yours goes, the higher tax bracket you’re in; this is called a progressive tax system.

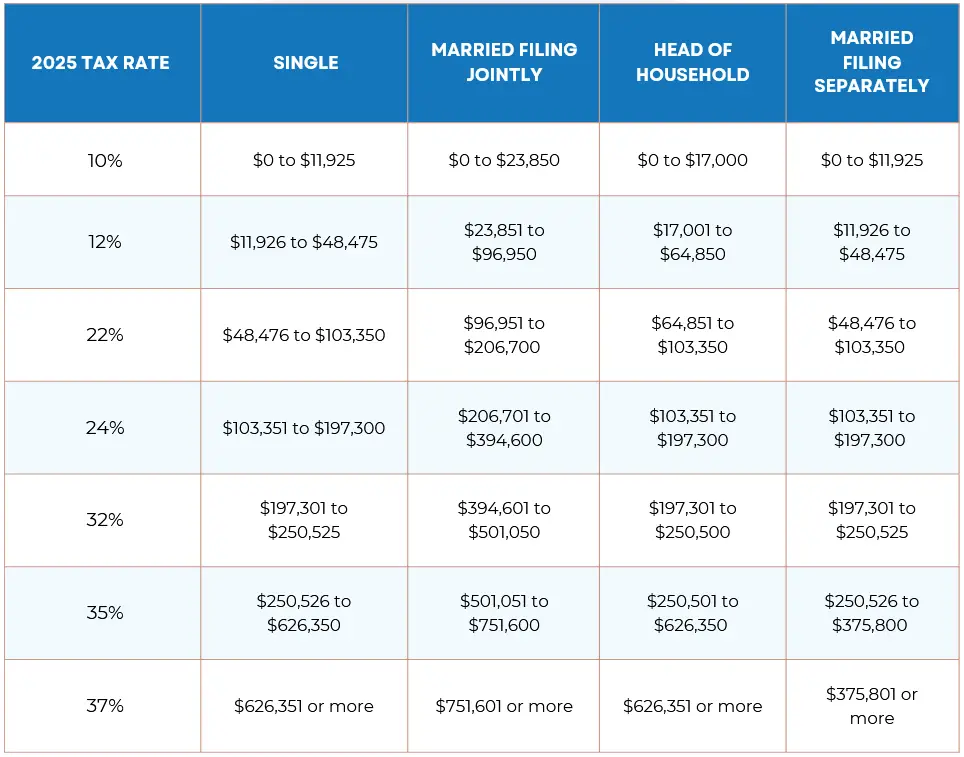

In 2024, there are a total of seven tax rates: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. Remember that, regardless of which tax rate applies to you, all of them are “marginal rates”, which means they won’t be applied to the totality of your income but a fraction of it.

How Do Marginal Tax Rates Work

As part of the progressive tax system, different parts of your income will be taxed at increasingly higher rates depending on which “tax brackets” they fall into. It is important to remember, for the sake of the following examples, that the marginal tax rate does not apply to your entire income; only to the specific portion of your taxable income that falls into the bracket. Here’s an example of how it works.

Let’s say you are a single filer and have an income of $100,000 for the year 2024. Now, following the tax brackets set out by the IRS, your taxes under the progressive tax system would look like this:

| Tax rate |

Income For Single Filers |

| 10% |

$0 to $11,600 |

| 12% |

over $11,600 to $47,150 |

| 22% |

over $47,150 to $100,525 |

Now, we do the following calculations:

1. The first $11,600 is taxed at 10%.

11,600 x 0.10 = 1,160

2. Next, the amount of money from $11,601 to $47,150 is taxed at 12%.

35,550 x 0.12 = 4,266

3. The remaining amount of your income (from $47,151 to $100,000) is taxed at 22%.

52,850 x 0.22 = 11,627

4. The total tax, then, would be calculated as follows:

$1,160 + $4,266 + $11,627 = $17,053

A common misconception is that, if your income pushes you into a higher tax bracket, that means the totality of your income will be taxed using that rate and taking less money home at the end of the day; only the income which falls into each bracket will be taxed using the corresponding rate, not your entire income. It seems basic, but misunderstanding this principle of the progressive tax system can lead you to make uninformed financial decisions.

Marginal Tax Rate Vs. Effective Tax Rate

Your effective tax rate is an average of the total taxes paid on your overall income, AKA the average tax rate you pay on your total income. This type of tax rate refers only to your federal income taxes and not state, sales, property, or local taxes you might pay.

To calculate your effective tax rate, all you have to do is divide your total tax by your total income. By following the example we used in the previous section, a taxpayer would calculate that effective tax rate as follows:

17,053 ÷ 100,000 = 0.17053 or 17% (after rounding down).

Flat Tax Rate Vs. Progressive Tax Rate

Just for comparison purposes, let’s look at what a flat tax system is and how it differs from progressive taxes. In a flat tax system, a single tax rate is applied to all taxpayers, regardless if they have high or low income; the flat tax rate also eliminates all deductions and exemptions, and most don’t tax income from capital gains, dividends, and others.

There are many proponents of using a flat tax system for the U.S., but critics of this proposal argue that implementing such a system would only serve to increase the burden of taxes on the low-income population.

There are other forms of flat taxes that are not income tax, such as the sales tax; it’s considered flat because everyone who buys the same product pays the same price for it, regardless of their income level.

Other Types Of Taxes

Income tax

Income tax is, simply put, the tax that the government imposes on the income you generate. You, as a taxpayer, must file your annual tax return in which you report all forms of taxable income as well as any deductions, credits and exemptions to lower your tax liability.

- Federal income tax: The word “taxes” alone usually means that someone is talking about federal taxes. In the U.S., federal taxes are regulated by the IRS and are used to fund the federal government. A progressive tax system is used, meaning that your income will be taxed at a progressively higher rate using a tax bracket system.

- State income tax: State income taxes can look very different from one another, with some having a progressive tax system like the federal government, while others have a flat tax system for all income levels.

- Local income tax: Local income taxes are something that most states usually do without, and even in states that do have them they’re usually imposed at low rates. Some use the same definitions as the state they’re in, while others define them with modifications.

Sales tax

The sales tax is imposed on the sale of goods and services, with the rate varying by state and even by locality. The sales tax is not considered a federal tax as it’s imposed at varying rates depending on where you are.

Property tax

An example of local tax, property tax is paid by the owners of real estate within a jurisdiction, with the amount of tax owed being a percentage of the value of the asset.

Corporate tax

A corporation’s profits are taxed at 21% of their taxable income, which is (in a very simplified manner) their revenue minus expenses. As you can imagine, there are also plenty of ways corporate taxes can be lowered; deductions, subsidies, loopholes, you name it.

Determine Your Marginal Tax Rate

There really is no easier way to determine your marginal tax rate than to look at the tax brackets and compare them to your taxable income. Remember that there are seven income tax rates that range from 10% to 37%.

How Are Tax Rates Determined

Your marginal tax rates will be determined by the following factors:

Income Level

The first factor that will be used to determine your tax rates is your income level. As we mentioned before in this article, your income level will be used to determine the highest tax bracket in which you’ll fall. Currently there are seven different tax rates, each applying to only the part of your income which falls in a specific range.

If you earn $1 million per year, your maximum tax bracket will be 37%; this means that every dollar above $539,900 that you made that year will be taxed at 37%. Since that is the highest bracket, it doesn’t matter if you made $1 million or $100 million, the 37% tax will apply to every dollar above that $539,900 mark.

Deductions, Exemptions And Credits

Tax deductions, exemptions, and credits can all reduce your tax liability by different percentages and amounts. Let’s go over each one:

- Tax deduction: Deductions are expenses you have made during the current tax year that you can then subtract from your taxable income. There are two ways to do this, a standard deduction that reduces your tax liability by a flat amount, and itemized deductions for a long, long list of specific expenses. It’s your responsibility as a taxpayer to know which type of deduction is more advantageous for you.

- Tax exemptions: Any sort of income or transaction that is free from taxes (at either the federal, state, and local levels) is considered tax-exempt. On a personal level, most taxpayers are entitled to exemptions that, much like deductions do, reduce the taxable income on your tax return.

- Credits: Unlike exemptions and deductions, which only reduce your taxable income, credits will directly reduce your tax liability — that means, the total amount of money you owe to the IRS. In other words, a $100 deduction or exemption means that you have $100 less on which to pay taxes, but a $100 credit means your tax liability is reduced by that same amount, full stop.

Filing Status

Your filing status is what defines which type of tax return you will fill when it comes time to file your taxes. There are currently five main filing statuses: single, married filing jointly, married filing separately, head of household, and surviving spouse. You have to be careful with the status you choose because it will affect the income ranges of your tax brackets, deductions and credits you can claim.

Each status offers its own tax advantages (yes, even single filing), so it’s not just about which one makes the tax number go lower at first glance.

Single Filer Tax Rates

Single filer is any taxpayer who is unmarried, divorced, registered domestic partner, or legally separated but still living together. Overall, taxpayers filing as single will have lower income limits on exemptions and credits.

Married Taxpayers Filing Jointly (Or Eligible Surviving Spouse)

Married individuals can file their tax returns jointly along with their spouse. This means reporting both incomes, deductions and other shared assets in a single tax return, which provides bigger tax refunds and (sometimes) lower tax liabilities.

Should one of the spouses’ sadly pass away, the surviving spouse (hence the name) can carry on filing for that same year and two additional years afterwards.

Married Filing Separately

Legally married couples can file their tax returns separately rather than combining their income on a joint return. This status can sometimes lead to a higher tax bill since many tax credits and deductions are reduced or unavailable. It can also be a strategic choice if one spouse prefers to be solely responsible for their own tax liability.

However, before choosing this status, it’s important to compare your potential tax outcomes with filing jointly to ensure you’re making the most tax-efficient decision.

Head of Household

Filing as head of household provides valuable tax benefits, including a higher standard deduction and lower tax rates than those filing as single. To qualify, you must be unmarried (or considered unmarried by IRS rules), have paid more than half the cost of maintaining your home, and have a qualifying dependent living with you for more than half the year.

This status is especially beneficial for single parents or those supporting a dependent, as it can significantly reduce taxable income. If you meet the qualifications, filing as Head of Household can put more money back in your pocket compared to filing as Single, so it’s worth checking if you’re eligible.

Qualifying Surviving Spouse

This is a status that is designed to help individuals who have recently lost their spouse by allowing them to continue receiving some of the tax benefits of filing jointly for up to two years after their spouse’s death.

To qualify, you must have a dependent child and not have remarried during the tax year. This status provides a higher standard deduction and often results in a lower tax rate compared to filing as Single.

The qualifying surviving spouse status serves as a financial cushion during a difficult time, making the transition easier while you adjust to filing taxes on your own. If you qualify, it’s a good way to minimize your tax burden and maintain financial stability.

Nick Charveron

Nick Charveron is a licensed tax practitioner and Partner & Co-Founder of Community Tax, LLC. As an Enrolled Agent, the highest tax credential issued by the U.S. Department of Treasury, Nick has unrestricted practice rights before the IRS. He earned his Bachelor of Science from Southern Illinois University while serving with the U.S. Army Illinois National Guard and interning at the U.S. Embassy in Warsaw, Poland. Based in Chicago, Nick combines his passion for finance and real estate with expertise in tax and accounting to help clients navigate complex financial challenges.