Key Takeaways

- Marginal tax rates are the tax rates that you pay on the highest dollar of your income. In a progressive tax system, the tax rate increases along with your income.

- Your taxes are calculated at different rates based on which tax brackets your income falls into.

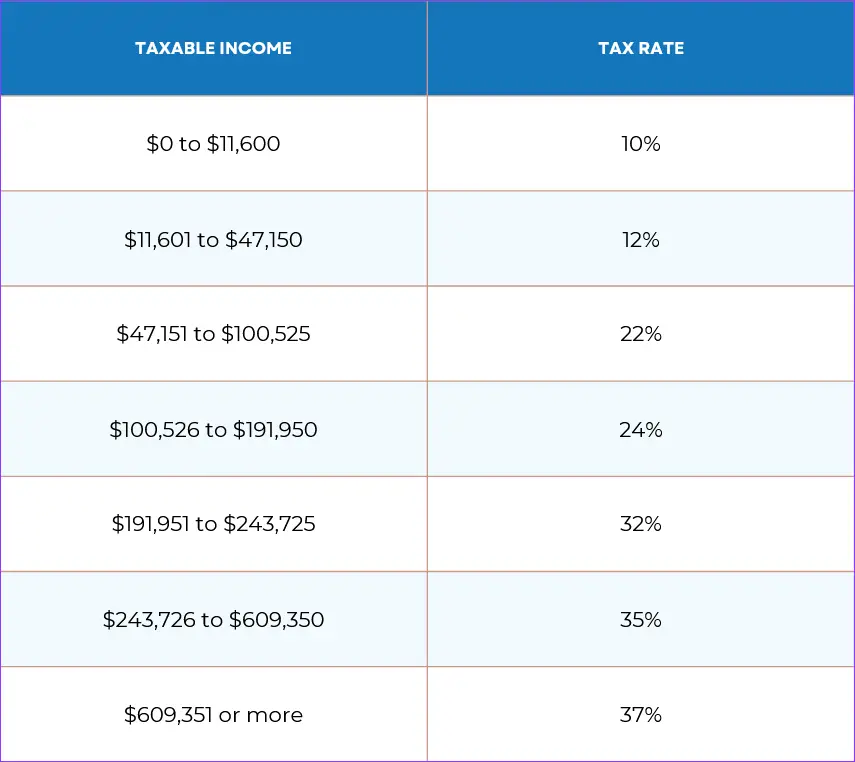

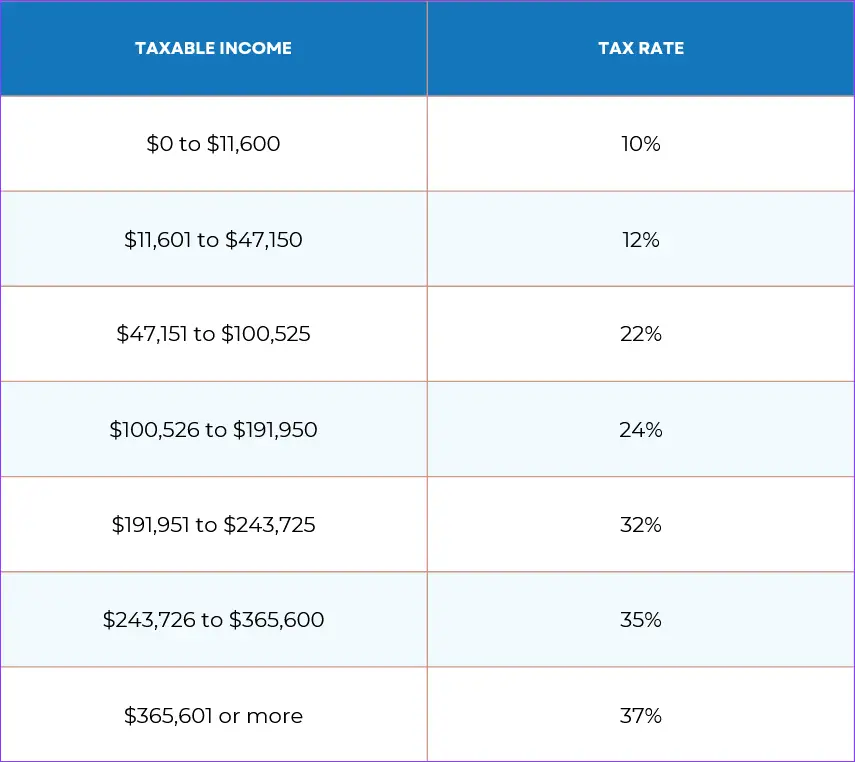

- For 2024 and 2025, there are seven marginal income tax brackets: 10%, 12%, 22%, 24%, 32%, 35%, and 37%.

- Marginal tax rates are part of a progressive tax system. The U.S. federal government uses a progressive tax system, while some states use a flat tax rate.

- You don’t pay the highest tax rate for your whole income, only the part of it that crosses the bracket’s threshold.

The marginal tax rate is what you pay on your highest dollar of taxable income. You’ve probably heard (and used) the term many times in the past, but what does it mean?

In a nutshell, the marginal tax rate is the highest tax rate that applies to the highest portion of your taxable income. And how does the IRS determine how much that amounts to? Well, through federal income tax brackets; these are in turn determined by your filing status and how much you earned during the year.

RELATED: Common Tax Questions & Answers

Your filing status is determined by your marital status on the last day of the year, but there’s a few caveats. For example, only married people and domestic partners can file a joint tax return (usually referred to as “filing jointly”), but they can also choose to file an individual tax return (one for each of them, of course). Your filing status also determines your filing requirements, standard deduction amount, and your eligibility for certain credits.

The marginal income tax rate system is known as a “gradual tax schedule.” That basically means: as you make more money, you pay more tax. Your marginal tax bracket is the highest tax rate that you will pay on your income. For tax years 2024 and 2025, there are seven tax brackets for each filing status: 10%, 12%, 22%, 24%, 32%, 35%, and 37%.

Find Your IRS Tax Brackets and Tax Rates

Many people do not understand their marginal income tax bracket and how it affects them. In turn, they can end up making financial decisions that are actually less beneficial in the long run. Here’s what you need to know about marginal tax brackets.

Tax brackets are adjusted by the federal government every year with the idea to keep up with inflation, since the rising cost of living would eventually put everyone into the highest tax brackets. Moving tax brackets continually up means that more of your income is protected as the years go by.

One of the most common misconceptions is that moving into a higher tax bracket (e.g., from a salary increase) means that all of your income will be subject to a higher tax rate. But this is actually untrue. For example, if you move from the 22% tax bracket to the 24% tax bracket, only the money that you earn within the 24% bracket is taxed at that rate.

2025 Income Tax Rates

Listed below are the 2025 individual income tax rates, organized by federal filing status.

Single

Married Filing Jointly or Qualifying Widow

Married Filing Separately

Head of Household

Understanding Marginal Tax Brackets

The marginal tax bracket system is a gradual tax schedule, which essentially means the more you earn, the more tax you pay. The amount of taxable income that you earn determines which tax bracket(s) you fall into. While it is the goal of many taxpayers to keep their income in the lower tax bracket, remember that the gradual tax schedule ensures that not all of your income is taxed at a higher rate.

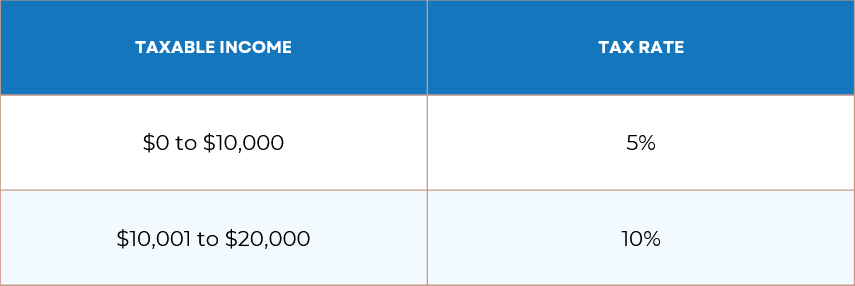

For example, let’s make up some round numbers to make this easier to understand. Suppose you have an income of $10,100 for this year. Let’s also imagine that the tax brackets are as follows:

Makes things simpler, right? You see, if you have a total income of $10,100, that means that it falls into two different income brackets: the first $10,000 fall into the 5% bracket, while $100 fall into the 10% bracket. Does this mean that your entire $10,100 income will be taxed at 10%? Not at all! It means that $10,000 of your income will be taxed at a 5% rate, while only $100 will be taxed at 10%.

The structure of federal income tax brackets was first implemented by the IRS in the early 1900s in an attempt to create a progressive tax system that would demand less from lower-income individuals. This system, plus a series of tax credits and tax deductions, have allowed nearly half of Americans to avoid owing federal income tax altogether [Source: The Tax Foundation].

If you understand marginal income tax brackets and how they work, you can use this knowledge to help save money on your income taxes. If you are close to one of the marginal tax bracket limits, you can actually avoid moving into the next tier by controlling the amount of income that you earn. However, it’s recommended that you run the numbers and consider your particular situation before implementing a specific tax strategy, because owing less tax means earning less income.

In order to properly file your federal income tax return and pay any tax that you owe, it is necessary to understand your income tax bracket, your filing status, and which income tax rate(s) apply to you.

Effective Tax Rates

Your effective tax rate is the percentage you paid on your annual income to the IRS. While not particularly relevant to your tax return process, it can help you budget for the next tax year. It’s also known as the “average tax rate”, which makes it pretty self-explanatory.

Calculating your effective tax rate is actually very easy, all you need is two numbers: Your annual income (which is your gross income before taxes) and your total tax liability (which is what you paid in taxes. Now you just take your tax liability and divide it by your gross annual income, then multiply the result by 100. This final number is the percentage of your income you paid in taxes.

The Final Word On Marginal Tax Rates…

Knowing the difference and relation between marginal tax rates and income tax brackets can help you make better financial decisions in the future. It’s also important to remember what a progressive tax system means, and how the totality of your taxable income will not be taxed at the highest tax rate; many people believe that, so they make poor financial decisions that can end up with them paying more in taxes, or at the very least makes their filing process all the more complicated.

Marginal Tax Rates And Tax Brackets: FAQ

1. What is a marginal tax rate?

Marginal tax rates are the percentages at which taxes are applied to specific “parts” or sections of your taxable income. They are all based on the tax brackets in which your income falls into, and they grow higher the more income you make. It is key to remember that your entire income is not taxed using one single tax rate.

2. What is a tax bracket?

In a progressive tax system like the one we have in the U.S., tax brackets are used to divide your income into different ranges that will be taxed at specific rates. As your income goes higher, different portions of it will reach higher brackets as well. Let’s say your income falls into three different tax brackets; that means those three portions of your income will be taxed at three specific rates assigned to those brackets.

3. If my income falls into a high tax bracket, does it mean I’m getting taxed more overall?

No. Only the portion of your income that falls into the tax bracket will be taxed at the rate specified in that bracket. This means that only the amount that crosses over that bracket’s threshold will be taxed at a higher rate, with the rest of your income below that threshold will be taxed at a lower rate.

4. What’s the difference between marginal tax rates and effective tax rates?

Marginal tax rates apply only to specific parts of your income, while the effective tax rate (AKA average tax rate) is the total tax you pay expressed as a percentage. An average effective tax rate will typically be lower than the highest tax rate applied to your income.

5. How do I find my tax bracket?

Tax brackets are determined annually by the IRS, and are directly impacted by income and filing status. The IRS website is your best bet to find which tax brackets your income will fall into once you know what your income is and under what status you’ll file your tax return.

6. How can I bring my income into a lower tax bracket?

The best way to lower your taxable income (thus preventing it from crossing over into higher tax brackets) is to take advantage of deductions and credits, and to contribute towards approved retirement accounts.

Jacob Dayan

Entrepreneur • CEO Community Tax, LLC

Jacob Dayan is the CEO and co-founder of Community Tax LLC, a leading tax resolution company known for its exceptional customer service and industry recognition. With a Bachelor’s degree in Business Administration from the University of Michigan’s Ross School of Business, Jacob began his career as a financial analyst and trader at Bear Stearns and Millennium Partners before transitioning to entrepreneurship. Since 2010, he has led Community Tax, assembling a team of skilled attorneys, CPAs, and enrolled agents to assist individuals and businesses with tax resolution, preparation, bookkeeping, and accounting. A licensed attorney in Illinois and Magna Cum Laude graduate of Mitchell Hamline School of Law, Jacob is dedicated to helping clients navigate complex financial and legal challenges.